Money (I): The Past of Trial and Error

Innovating the institution of exchange to modern centralized money

If you want to really understand money, you’ve got to take a detour into human biology and anthropology. Stick with me here. Humans, when we’re born, we’re basically useless. We’re one of the most helpless mammals at birth—can’t walk, can’t eat by ourselves, can’t even regulate our body temperature properly. Why? Because our brains are still developing, and we need this whole elaborate support system of caregivers1 feeding us, keeping us alive, and bonding with us, thanks in part to oxytocin, that nifty little “love hormone”. Babies also come with digestive and immune systems that aren’t fully operational, so they need breast milk to make up for all those missing nutrients and antibodies.

What’s that got to do with money? Well, this whole thing tells us something about humans: we’re social creatures2 from day one. We rely on others not just to survive but to thrive. For thousands of years, family and community networks have been essential for sharing and exchanging resources—and even more so today. Think about it: almost everything you rely on involves a chain of exchanges before it lands in your hands or serves your needs.

This isn’t just about swapping food and favours—over time, it shaped our ability to think abstractly and communicate in symbols. You know, like...words. And, eventually, like...money.

Language was actually humanity’s first symbolic exchange system—every culture has one, and they’re all about communication and cooperation3. It’s what lets us do the complicated social learning thing, passing down knowledge, skills, and cultural norms across generations in ways no other species comes close to pulling off. Money? Same thing, but for enabling the exchange of resources4. We needed something to track who owes what to whom, because bartering goats for grain only gets you so far.

Different communities have always juggled multiple exchange systems at once, each shaped by its own process of social convergence. Over time, these systems evolved, which is why we’ve gone from gift economies and bartering to swiping your credit card for a latte. The medium form and technologies changed, but the core idea—a shared belief in value exchange—stayed the same.

So, where did this all start? Let’s take a look at the major milestones in the history of money.

Love diving into these topics? Join a community of critical thinkers like you, engaging around the workings of money during this transformative “Bretton Woods Moment.”

Join The Hard Money Project Community:

Don’t forget to subscribe for project content updates in your inbox!

1. The Gift Exchange before barter

Let’s go back to the Paleolithic era—2.5 million to 12,000 BC—when humans were still in the “figuring out life” phase. No cities, no farms, just small nomadic groups hunting and gathering around small communities (hunter-gatherer societies). Civilization or large-scale complex economies as we know it? Not even close. But these early humans did have something going for them: a “gift economy”.

Here’s how it worked: you’d team up with the rest, and given your hunting skills, you’d provide meat from the hunt for the community, while others would handle different tasks—without expecting anything in return right away. It wasn’t bartering—nobody was trading furs for fish. It was more about fostering social bonds and trust5. Maybe one day they’d return the favor, or maybe not. But the point was that keeping the group alive mattered more than hoarding resources.

This wasn’t just out of altruism; it was also practical. Helping each other increased everyone’s chances of survival. If you were selfish, you might find yourself on the outside when things got tough. So in a way, it was like the first form of social insurance—no contracts, no rules, just a mutual understanding that if you help now, you’ll likely get help later.

These exchanges weren’t transactional in the way we think of trade today. Nobody was keeping a ledger of who owed what. It was all about maintaining relationships. Money and credit? They came much later. This trust and free reciprocity, as shown in Fig. 1, were basically their original currency for enabling exchange, helping glue the community together and keep everyone alive.

2. Barter: bridging the exchange gap to money

So, fast forward to around 12,000 BC, and we hit the Neolithic Revolution—a fancy way of saying, “we figured out how to farm”. Humans got a bit more sophisticated—or at least stayed put long enough to start growing crops. Instead of wandering in search of food, people in the Fertile Crescent6 learned how to cultivate it. Agriculture led to surplus, and surplus meant they finally had more than they could eat, drink, or stash in a cave. That’s when trade started expanding and getting interesting.

At first, this was still pretty cozy. You’d exchange goods within your community—maybe you gave your neighbor some grain, and they’d promise to fix your roof. It’s all pretty informal, but that worked in tightly-knit groups where everyone knew everyone. Eventually, though, you start exchanging goods with foreign communities and circles with strangers where trust is not as direct or reciprocal. Suddenly, your neighbor’s roof-fixing skills weren’t going to cut it anymore, so you turned to a barter system instead. Now, you’re swapping your surplus grain for someone else’s metal tools or textiles in another economy. Simple enough, right? Wrong.

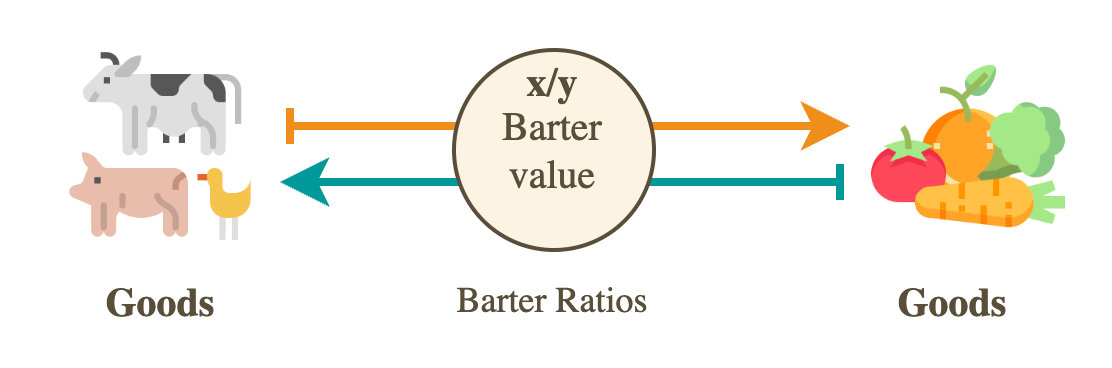

Barter sounds easy, but it’s a logistical headache. It all depends, as shown in Fig. 2, on the “double coincidence of wants” at the resulting barter ratios—meaning you’ve got to find someone who has exactly what you want and also happens to want exactly what you have. Good luck with that. Imagine trying to buy groceries today with a goat and hoping the cashier needs one.

Now, barter economies didn’t completely replace gift economies; they existed alongside them, along with these proto-credit systems where people basically said, “I’ll pay you back later”. Because, let’s be real, farmers didn’t always have their harvest ready when they needed something. Take Mesopotamia, around 6000 BC. Communities practiced reciprocity and redistribution, with Temples acting like communal warehouses to manage these IOUs7 claims for future goods. In a way, they were like early banks, helping farmers get through lean seasons by lending grain and expecting repayment after the harvest.

Fast forward to around 3400 BC, the Sumerians invent cuneiform writing8—game changer. Now, they could actually record creditor-debtor relationships denominated in a specific product or service, in economies heavily driven by barter exchanges. Suddenly, barter became more sophisticated, like an early banking system. Farmers would agree on future deliveries of grain or other goods, and it was all written down, so nobody could forget who owed what. These records, typically stored in temples (because where else?), kept things organized.

And this concept—recording transactions instead of physically moving goods—spread quickly. Barter had evolved, but it was still a pain, and people were starting to think, "There’s gotta be a better way to do this”. By 3000 BC, Mesopotamia and Egypt had more formal barter systems with initial commodity money forms, with long-distance trade happening across the Mediterranean. By 500 BC, trade had moved beyond just grain and wool—now they were dealing in tin, silver, and gold, with Phoenicians setting up shop in every port from Tyre to Carthage. You know, the kind of commodities that gets future bankers and central banks excited.

3. Money: the efficient exchange facilitator

Gift economies, barter systems, and early money weren’t mutually exclusive. People kept mixing and matching based on whatever worked best in their particular context. But slowly, money emerged as the main tool for exchange, especially as it solved the annoying “double coincidence of wants” problem. As shown in Fig. 3. Monetary economies, purchasing power is basically the relationship between money and the total value exchanged, with prices acting as a nice, neat representation of those relationships on a per-unit basis.

People eventually got tired of lugging around grain sacks and metal ingots to settle their debts. The invention of money wasn’t some grand, carefully orchestrated plan. It was more of a slow, messy convergence where certain commodities—like silver and gold—started catching on because, let’s be honest, they were durable, shiny, easy to melt and divide, and didn’t rot.

Barley, measured in “sila”, was great for your daily bread and small trades, but for high-value exchanges? Silver, measured in “shekels” and “talents” was the better choice—it didn’t spoil, and it looked good doing it. Pretty soon, Mesopotamians were using it for long-distance trade, and voila—you have the first currency system.

Eventually, this fascination with metals led to a breakthrough around 600 BC in Lydia: coins. Lydian king Alyattes (reigned c. 619-560 BC) figured out that if you standardize chunks of metal—electrum, a gold-silver alloy—you can stamp them with an official mark, and voilà, you’ve got the first standardized coins and unit of account. Suddenly, you didn’t need to weigh or test the purity of metal at every transaction. You had trust in the currency because, well, it had the royal stamp of approval. And once you’ve got coins, taxes follow—because, naturally, governments want their cut, and they’re not interested in getting paid in barley.

Coins spread across the Mediterranean, showing up with different designs and symbols. The Greeks, being the Greeks, slapped their gods on the coins, while the Romans in the 1st century BC, always practical, named their money after the goddess Juno Moneta, whose temple housed their mint. The term “money” itself? Yep, that’s where it comes from.

But Rome wasn’t just about coins. They took the old Mesopotamian idea of credit and formalized it into promissory notes, receipts, and other early representative forms of the underlying money (representative money9), as claims on physical commodities stored in warehouses. It was a handy system, especially if you didn’t feel like hauling around a ton of metal.

But the shift to representative money, paper tokens backed by metal commodities, didn’t really take off on a broad scale until China came into the big picture. By the Tang Dynasty (618-907 CE), merchants were using “feiqian”, or “flying money”, essentially private promissory notes backed by metal deposits, typically copper coins or silver. Fast forward to the Song Dynasty (960-1279 CE), and you get the first government-issued paper money, the “jiaozi”. Instead of schlepping coins across the Silk Road, you could now carry a slip of paper that said, “I’m good for the cash”.

In Europe, though, they didn’t jump on the paper money bandwagon until much later, mostly because cultural and economic exchange with China was pretty limited back then. By the 12th century, the Knights Templar figured out that lugging coins, silver deniers or gold bezants across continents was a hassle, so they started issuing letters of credit to pilgrims headed to the Holy Land. Basically, the medieval version of a traveler’s check: you hand over your silver, they give you a letter, and you can cash it in at one of their outposts. Not quite cash, but close enough.

And then there were tally sticks in 12th century England for debt and credit management denominated in their silver coins. Picture this: a wooden stick, notched to show how much money you owed. The stick gets split in two—one half for the debtor (the “foil”), one for the creditor (the “stock”). It’s basically the world’s least efficient, yet surprisingly fraud-resistant, spreadsheet—perfect for the Exchequer to track transactions, debts, and, yes!, taxes. A milestone in the history of debt and credit record-keeping.

By the late 15th century, though, things started getting serious in 1494 with Luca Pacioli and double-entry bookkeeping advancements. Every transaction had to balance—a debit here, a credit there. The Medicis in Florence ate this up, using it to manage vast payment and credit networks, basically turning private banking into an international power move. Then the Fuggers came along and upped the ante, becoming the go-to financiers for European monarchs. They pioneered private fractional reserve banking, lending out more credit than they had in actual reserves of commodity money.

So, by 1609, Europe’s financial system was a bit of a mess. Multiple currencies, merchants lugging around sacks of silver and gold, and no real central bank to organize things. Enter the Bank of Amsterdam. This bank was essentially a giant safety deposit box where merchants could store their gold, silver, and coins, and in return, they’d get “banco guilders”—paper money fully backed by the metal sitting in the vaults. Simple, secure, and revolutionary. It quickly became a clearinghouse for large-scale international trade, helping to stabilize the chaotic currency situation across Europe. Everyone loved it.

But here’s the thing: the Bank of Amsterdam wasn’t exactly a central bank in the modern sense. It wasn’t “printing money” out of thin air by messing around with policy tools like interest rates. It was fully reserved, meaning it only issued as much money as it had in its vaults—until it didn’t. Fast forward to the 1780s, and the bank started secretly lending to the Dutch East India Company and the City of Amsterdam. Without maintaining enough reserves to back those loans, things started to fall apart. You can guess where this is headed: bad loans, not enough gold to go around, and a slow, painful decline.

But let’s rewind a bit. Before this implosion, the Bank of Amsterdam—and earlier practices from the Fuggers and other private banks—helped pave the way for a big leap in Western monetary history: the shift from private issuers to government-backed banknotes. Enter Stockholms Banco in Sweden, founded in 1656 by Johan Palmstruch, under royal charter from King Karl X Gustav. Palmstruch had a brilliant idea: Why not issue paper money? So in 1661, the first official European banknotes were born. These notes were backed by copper deposits and could be exchanged for their equivalent value. Sounds smart, right?

Well, it was, until Palmstruch got a little too enthusiastic and started issuing more notes than the bank had in reserves. People caught on—because they always do—and bam, a bank run. Stockholms Banco collapsed by 1667, but the damage was done (or rather, the innovation). Despite its short run, the bank introduced the world to state-backed paper currency, a major turning point that paved the way for governments to consolidate power over money—leading us to the modern central banks we know and...love?

Ultimately: Money is a story of trial, error, and convergence

If you look at the history of money, it’s basically one long story of power consolidation. Every new monetary innovation starts out as this cool, decentralized, grassroots thing—people swapping gifts, bartering goods, or using shiny metal tokens to settle their exchange and debts. But over time, as things get more complicated and societies grow, money tends to drift toward one inevitable conclusion: the centralization of power. Eventually, the people running the show (aka governments) step in, take over, and make sure they’re the ones in charge of the “money printer”.

It's like a law of nature: every time someone invents a cooler form of money, it ends up being co-opted by the powers that be. Gift economies? Nice idea, until the village elder starts keeping tabs on who owes who. Commodity money? Great, until the king decides he's in charge of the mint. Representative money? Fantastic, right up until the central bank enters the chat.

Once Stockholms Banco issued the first official banknotes, backed by copper deposits, it marked a huge turning point. Sure, there had been private issuers before that, but this was different—it was government-backed money, and that’s a big deal for modern money. The ability to print money on demand wasn’t just a nifty convenience for traders, it was a consolidation of power for governments. After all, when you control the money supply, you pretty much have the power to influence everything else on the other side of the money being exchanged…

Feldman, R., 2007. Parent–infant synchrony: Biological foundations and developmental outcomes. Current directions in psychological science, 16(6), pp.340-345.

A) John-Steiner, V. and Mahn, H., 1996. Sociocultural approaches to learning and development: A Vygotskian framework. Educational psychologist, 31(3-4), pp.191-206.

B) Greenfield, P.M., Keller, H., Fuligni, A. and Maynard, A., 2003. Cultural pathways through universal development. Annual review of psychology, 54(1), pp.461-490.

Tomasello, M., Melis, A.P., Tennie, C., Wyman, E. and Herrmann, E., 2012. Two key steps in the evolution of human cooperation: The interdependence hypothesis. Current anthropology, 53(6), pp.673-692.

Parry, J.P. and Bloch, M. eds., 1989. Money and the Morality of Exchange. Cambridge University Press.

Bird-David, N., 1990. The giving environment: another perspective on the economic system of gatherer-hunters. Current anthropology, 31(2), pp.189-196.

The Fertile Crescent is a historically significant region in the Middle East that spans modern-day Iraq, Syria, Lebanon, Israel, Palestine, Jordan, and parts of Turkey and Iran. It is characterized by its rich soils and crescent-like shape, making it an early center for agriculture and the rise of some of the world’s first civilizations, including Mesopotamia and ancient Egypt.

An IOU (short for "I Owe You") is a written acknowledgment of debt, representing a promise to pay a specific sum to the holder at a future date.

Cuneiform writing, developed by the Sumerians of ancient Mesopotamia around 3400-3000 BC, was used extensively for economic and administrative purposes, including exchange record keeping ledgers. These ledgers recorded transactions, debts, and credits in commodities such as grain, livestock, and silver.

Representative money refers to currency that represents a claim on a commodity of any type, commonly converged to gold or silver, that can be redeemed upon demand. It has no intrinsic value but derives its value from the commodity it represents, functioning as a certificate that can be exchanged for a specified amount of a physical asset.